March 16, 2021 | Amanda Williams, Joseph Howell Wood, Shant Mirzaians, Daniel Zawodny

The coronavirus pandemic has illuminated and exacerbated existing inequalities across many aspects of American life, including housing. As the economy shuttered and millions lost jobs, officials implemented eviction moratoriums that kept many people in their homes. At the same time, low interest rates and a scarcity of home listings created a real estate boom in cities across the United States.

“The bottom half of the population are the ones that lost their jobs as service workers, the entertainment workers. … The knowledge workers kept going. They kept going and their incomes didn’t take any hit at all. That’s why they can bid like crazy for houses because they didn’t suffer any loss,” said Dowell Myers, a University of Southern California public policy professor and an expert in demographic changes. “The pandemic has made every division greater, it’s highlighted every single division we have.”

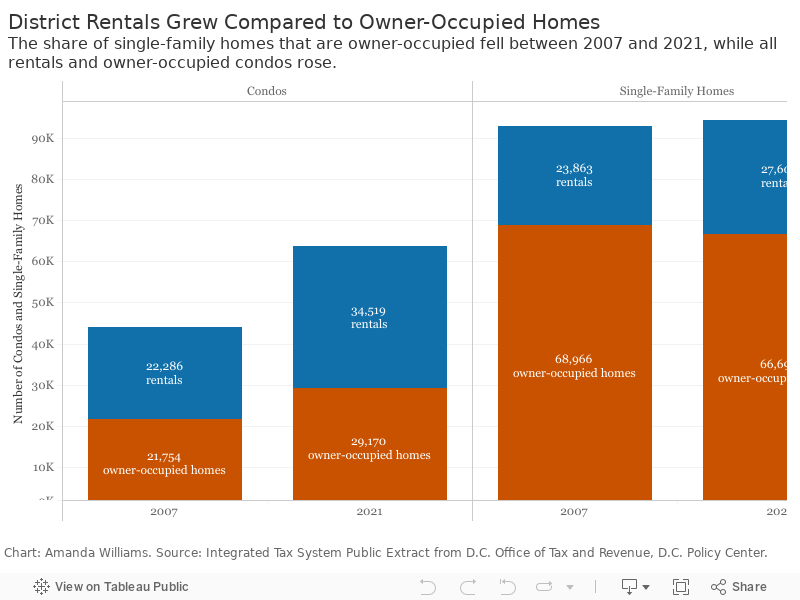

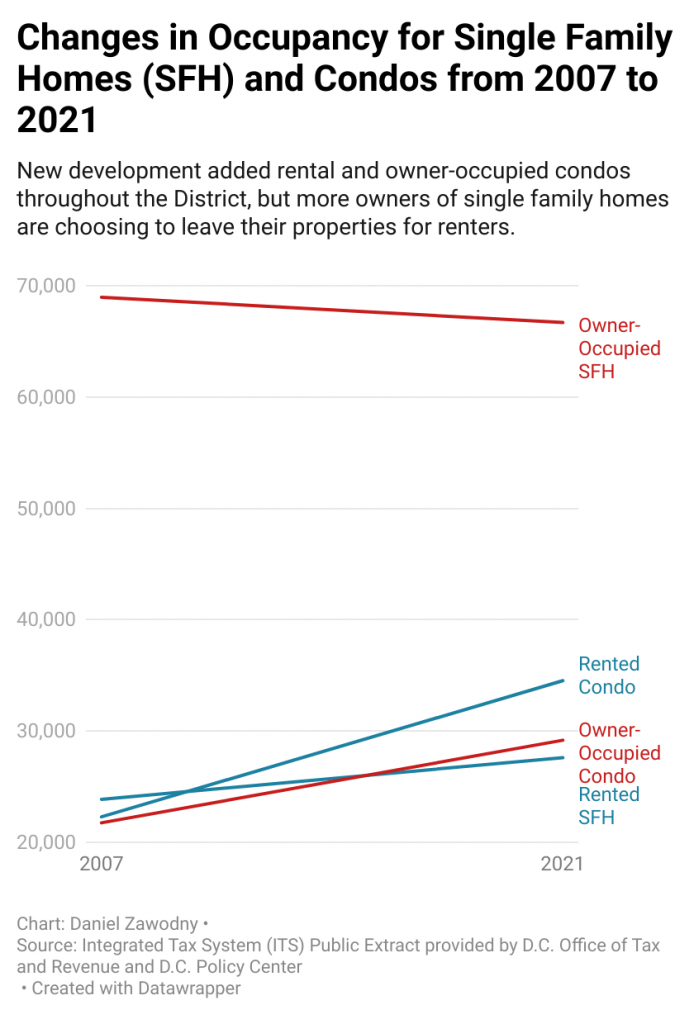

For a city like Washington, D.C., which has seen an increase in renters over homeowners since the Great Recession, the divide is even more stark. According to an analysis of real estate tax data, the number of single-family homes and condos being rented out instead of lived in by the homeowner grew by almost 35% between 2007 and 2021. Owner-occupied properties saw just 6% growth, primarily due to a jump in condos.

To capture only the housing options that buyers either choose to live in or rent out, rather than buy as a business investment, the analysis attempted to exclude properties with more than one unit as defined by the district’s tax code. The analysis looked at whether a property claimed the Real Property Homestead Deduction, a tax break that can be claimed only on a taxpayer’s primary residence, to decide whether it was likely rented out or owner occupied.

Both rentals and owner-occupied properties grew between 2007 and 2021, however rentals far eclipsed owner-occupied properties with nearly 16,000 rentals gained to a little over 5,000 owner-occupied properties.

Most of the growth between the two years — there were nearly 137,000 properties total in 2007 compared to almost 158,000 in 2021 — was due to the addition of nearly 20,000 condos.

While overall stock of condos and single-family homes increased, the share of owner-occupied single-family homes fell as more found their way into the rental market.

Joseph Edgar, real estate investor and CEO of the technology company TenantCloud, said these numbers reflect a nationwide trend, a shift he partly attributes to the Great Recession. He said the nation has struggled to supply housing for everyone who needs it.

“You just can’t take what we have right now and house all of the people that want to be here, which means we’ll have another ten years of just high demand. Now throw a pandemic in the middle of it, and single family rentals become the best investment of 2020,” Edgar said.

A 2018 report by Yesim Sayin-Taylor, Executive Director of the DC Policy Center, used tax and other public housing data to look at affordability and other major housing issues in the city.

“The city is richer and whiter, less inclusive, and more segregated,” Sayin-Taylor’s report found. “These changes are partly attributable to the composition of the city’s housing stock, and especially the scarcity of family-sized units affordable to low and middle-income families. The lack of housing options is pushing low and middle-income families out of the city and increasing economic segregation.”

When it comes to family-sized units, it found that middle-income families have been priced out by usually younger affluent singles and couples.

During the pandemic, that affordability gap has morphed into a chasm.

Sheena Saydam, managing partner at local real estate firm Saydam Properties Group, said housing in the Washington metro area has had such high demand recently that only the most affluent buyers can compete.

“We’re seeing as many as 30 offers on some homes, escalation clauses, $100,000 to $150,000 over the asking price,” Saydam said. “Now that’s not super common. I mean, it wouldn’t be uncommon to see a home sell for $20,000, $30,000, $50,000 above the asking price.”

With the pandemic came record low interest rates, prompting staggering growth in the market over a short time. The rest is what she calls the COVID effect: an eagerness to escape the close quarters of the city’s apartment and condo buildings now that many can work from anywhere with an internet signal.

That has led to a major increase in people looking to purchase single-family homes, particularly in the suburbs. She said the district’s higher-than-average incomes mean many of the buyers are able to compete because they can offer cash.

“We’re definitely seeing a lot of young people who have great jobs and they can afford to do this,” Saydam said. “The fact that they’re not going out so much to drink and eat and paying for their workouts, they are able to save up more money.”

The same cannot be said for all of the district’s residents.

According to Stout, a global investment bank and advisory firm, as many as 44,000 district families could be facing eviction this year. In an attempt to keep renters in their homes during the pandemic, the federal government instituted a moratorium on evictions.

The district’s order is tied to Mayor Muriel Bowser’s declared public health emergency and will allow evictions to resume 60 days after the public health emergency is over.

Lori Leibowitz, a Neighborhood Legal Services Program managing attorney representing low-income tenants, said what happens when the moratorium ends is up to those in power now.

“If we do not put significant resources toward helping tenants and landlords recover from this, then we’ll have a tsunami, a tidal wave of eviction filings — whatever weather analogy we are using,” Leibowitz said. “The other option is that we make a real plan, using a combination of federal and local money to make people whole and make people close to whole, so that tenants can stay where they are.”

In addition to the federal ban on evictions, the district’s government passed measures to address the back rent owed by low-income renters. These include a $1.5 million program for them to stay current on rent for as long as two years and an emergency rental assistance program to provide pay-outs in the short term to those who qualify, according to the district’s coronavirus housing resources website.

Georgetown University professor and researcher Eva Rosen agrees with Leibowitz that the city will face a backlog of eviction filings once the moratorium ends if more isn’t done.

She’s not so confident the city is ready.

“We have an influx of $200 million from the federal government that can be used for emergency rental assistance, but it’s sort of an open question as to whether or not we’re equipped to get that out as quickly as it needs to get out and to actually, again, prevent these evictions from going forward while that money is sitting in the bank,” Rosen said. “That’s a big concern for me.”

In December, Congress authorized $25 billion in emergency rental relief to help families behind on their payments due to the pandemic, $200 million of which has been allocated for the district.

For homeowners struggling to pay a mortgage, officials designing relief packages haven’t forgotten them either.

Early in the pandemic, the U.S. government allowed people with federally backed mortgages to apply for delayed payments during the pandemic. This forbearance program includes protections for tenants within those properties. Federally backed mortgages also benefit from a foreclosure moratorium.

In Washington, homeowners behind on mortgage payments can apply for a six-month loan from the city to put toward their monthly payment, according to the district’s coronavirus housing resources website.

“In many ways landlords are getting more protections, especially strong small landlords, are actually getting more protections than almost any other kind of small business during the public health emergency,” Leibowitz said. “And larger landlords were eligible for the Paycheck Protection Program loans. …. So I think that’s important to keep in mind when you’re thinking about landlords and evictions — that there are other resources available to protect them and their businesses, in addition to just getting money from their tenants.”

As a real estate investor, Edgar doesn’t see these as protections. He said there is a distinction between how assistance packages may affect smaller landlords compared to larger ones. While renters can receive forgiveness on rent, most of their landlords can only receive forbearance.

“Forbearance is a way to make it look like they’re helping people, but they’re just making a loan longer and making more money be owed to the bank,” Edgar said. “And I’m talking about the landlords that only have one or two properties — they’re really the ones asked to take the brunt of it.”

For Leibowitz, being a landlord is a business choice — having a home is not.

With interest rates rising again, Saydam said she expects a slow down in the housing market — though how affordable it may become is still a question. Given that homeownership is widely seen as a step toward building wealth, some wonder how long families will be able to afford the city living at all.

A 2020 Policy Center report also authored by Sayin-Taylor found that at the start of that year, roughly 40,000 households in the district could not pay more than $750 per month on rent to keep their expenses stable, but that fewer than 800 units in that price range were available.

Though Sayin-Taylor notes that rents in the city dropped over the last year as landlords fought to attract the tenants who hadn’t fled for bigger spaces and fewer crowds, she said the deals aren’t expected to last.

“We always think of rental housing as something we can use to both address affordability and create mixed neighborhoods, but we’re seeing that affordability is not necessarily coming from rental housing,” Sayin-Taylor said.

Sayin-Taylor said the number of families in the district grew since 2011, attributing the rise to improving schools and universal pre-K. With data showing the share of renters in the district has been increasing, she thinks the city should focus on holistic solutions to keep families from being priced out.

“If you don’t have any kids, you may be more comfortable spending 40% of your income on your housing. On the other hand, you may choose, ‘I’m going to live in a small building, because I want to travel, I want to buy art.’ But that is not true for families,” Sayin-Taylor said. “I think we need to be intentional in thinking about affordability as not just, ‘what is someone paying at any given period of time ’ — but how burdensome is it to live for that family in the city?’”

With a market trend toward rentals in one of the least affordable cities in the nation, Myers wonders if even those who could afford it will stay at all.